A Special Report by the National Center for the Middle Market and CBIZ

Executive Summary

What drives performance in today’s middle market? While industry, size and external conditions all matter, a more fundamental driver lies in how leaders make tradeoff decisions under pressure. Middle market companies operate amid persistent cost pressures, workforce challenges, regulatory complexity and ongoing economic and policy uncertainty. In this environment, performance is shaped by how deliberately leaders navigate tradeoffs and balance priorities, including growth versus profitability, cost versus quality, speed versus accuracy and short-term performance versus long-term value.

While robust growth has long been a hallmark of the middle market and a dominant strategic objective, the ways companies are pursuing it vary widely. Differences emerge in how leaders evaluate risk, allocate capital, invest in talent and technology and decide what to protect or sacrifice when resources are constrained.

MINDSET MATTERS

These variations manifest in four distinct decision-making mindsets that shape how leaders approach challenges and help explain why companies with similar size and market exposure often achieve different outcomes. Some mindsets emphasize protection and resilience, prioritizing margin discipline and risk preparedness. Others pursue growth through centralized innovation, disciplined expansion or decentralized acceleration. Each reflects a different way of balancing near-term pressures with longer-term ambitions.

While no single mindset defines success across all contexts, innovation-oriented approaches are more often associated with stronger growth and greater confidence. Of course, the fundamentals of execution matter, too. Leaders who bring clarity and purpose to decision-making and effectively manage tradeoffs will be best positioned to operate amid uncertainty, navigate growth and maintain performance over time.

ABOUT THIS REPORT

To better understand the decision patterns underlying performance and business outcomes, The National Center for the Middle Market collaborated with CBIZ, a leading national professional services advisory firm and The Ohio State University Fisher College of Business faculty member, Dr. Jay Anand. As the Dean’s Distinguished Professor of Strategy, Dr. Anand consults companies all over the world and has been referenced in many notable publications such as The Economist, Financial Times, Forbes, New York Times and Wall Street Journal.

This research sought to examine in greater detail how middle market leaders make strategic choices and evaluate competing priorities. We studied what they prioritize and protect under pressure, and how they respond when tradeoffs are unavoidable. The goal was to move beyond sentiment and reveal the operational math of running a business through uncertainty.

This report is based on a 15-minute self-administered online survey fielded in December 2025 to 400 middle market business leaders and decision-makers from companies with annual revenues between $10 million and less than $1 billion. The sample includes respondents from three key industry segments: consumer and industrial products (N=208), construction (N=105) and real estate (N=87). A working research team, including experts from the center, Fisher College of Business faculty, CBIZ and other subject-matter specialists, designed the survey questions.

Insight 1

Four distinct decision-making mindsets shape middle market performance.

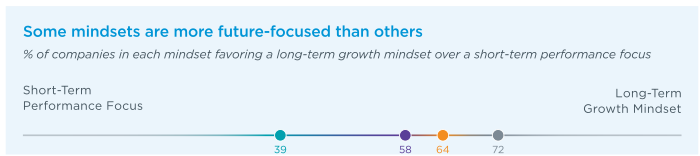

Since the center launched the Middle Market Indicator barometer study in 2012, the middle market has consistently outpaced both smaller and larger companies on critical performance metrics, including year-over-year revenue and employment growth. Further, middle market companies have historically recovered more quickly and more fully from economic setbacks. However, the specifics of how middle market companies achieve performance wins vary widely. Our research suggests four distinct decision-making mindsets or patterns, with significant differences among groups, particularly in how each balances short-term performance needs with long-term growth objectives.

1. DISCIPLINED GROWERS

A third of middle market companies approach growth with a strong focus on profitability. For this group, controlled, centrally managed expansion leads to high performance; they grow only when it makes sense from a margin perspective, thereby avoiding faster, riskier scaling. While most Disciplined Growers claim a long-term growth mindset, 42% of these companies prefer a balanced approach that equally considers short-term gains. Confidence levels are somewhat lower than in their more innovation-focused peers.

Representing 33% of survey respondents, Disciplined Growers demonstrate:

-

Disciplined, centrally managed growth

-

A focus on profitability and protecting margins

-

Strong revenue growth, but slower employment growth

2. PERFORMANCE PROTECTORS

Approximately one-third of middle market companies prioritize profitability and constrain growth to limit downside risk, relying on cost control and risk management while often deferring infrastructure and cybersecurity investments. They are the most likely group to prefer a balanced approach to short-term performance and long-term growth, and they are the only group with a meaningful proportion of companies (17%) choosing immediate gains over future value. Within this group, risk is well controlled, but growth initiatives, innovation and workforce expansion are often deprioritized. Confidence in future performance is lower than in other mindsets.

Representing 32% of survey respondents, Performance Protectors demonstrate:

3. CENTRALIZED INNOVATORS

Approximately one in five companies is a Centralized Innovator. These companies confidently pursue innovation-led growth bets, investing in talent and technology and accepting risk and margin pressure to accelerate scale. They are fast-moving, maintaining centralized control over decision-making to drive alignment, often at the expense of local autonomy. This group is the most likely to take a forward-looking approach to growth, with nearly three-quarters of Centralized Innovators favoring long-term goals over short-term performance. They are the most confident in their future performance.

Representing 18% of survey respondents, Centralized Innovators demonstrate:

-

Heavy investments in talent and technology

-

Centralized decision-making

-

A future-focused mindset and high confidence

4. DECENTRALIZED ACCELERATORS

This group of growth-first companies aggressively prioritizes innovation and accelerated scaling. These businesses invest heavily in talent and fully empower their people to make decisions in the pursuit of responsiveness, innovation and rapid growth. They accept risk and margin pressure to scale quickly and rely on both their workforce and automation to grow capacity. Decentralized Accelerators are the smallest group, representing 17% of middle market companies.

Representing 17% of survey respondents, Decentralized Accelerators demonstrate:

CERTAIN MINDSETS ARE MORE COMMON IN SPECIFIC INDUSTRIES OR REVENUE BANDS.

Decision-making mindset, rather than industry or revenue alone, shapes how middle-market companies manage opportunity and risk. These mindsets do cluster by sector and size, influenced by industry dynamics, operating complexity (capital intensity, margin pressure, regulatory exposure, workforce structure) and company scale. As a result, certain industries tend to skew toward particular decision-making styles, reflecting both structural realities and leadership norms within those segments. For example, according to the research:

- Construction companies over-index as Performance Protectors, consistent with an environment defined by project-based work, margin sensitivity and heightened exposure to cost volatility and execution risk.

- Real estate companies most commonly align with the Disciplined Grower mindset and are least likely to be Centralized Innovators, underscoring a preference for measured expansion and returns-driven decision-making over centralized innovation strategies.

- Consumer and industrial products companies are the most evenly distributed across the four decision-making approaches. While they are most likely to be Disciplined Growers, this group has the largest proportion of Centralized Innovators of any industry in this study, reflecting a strong emphasis on investment in product development, process improvement and innovation-led growth.

Company size also correlates with distinct decision-making mindsets.

- The smallest middle market companies in the study, with revenues between $10 million and $50 million, are notably most likely to fall into the Disciplined Grower category, where decision-making is more tightly linked to near-term profitability and risk management.

- In contrast, the largest middle market companies—those with annual revenues between $100 million and $1 billion—are more likely than their smaller peers to be Centralized Innovators or Decentralized Accelerators, the two groups that most aggressively pursue longterm growth. Their greater scale appears to provide both the capacity and the confidence to prioritize future-oriented investments.

- Companies in the middle revenue tier ($50 million to $100 million) appear to reflect a transitional stage where leaders must balance immediate performance pressures with emerging growth opportunities.

MIDDLE MARKET PERFORMANCE IS NOT DRIVEN BY A SINGLE “RIGHT” APPROACH.

The decision-making mindsets provide a framework for understanding why middle market companies approach critical business performance decisions differently, even when operating in similar markets. As organizations scale, many gain both the resources and the perspective to shift from protecting performance to deliberately shaping their long-term trajectory, evolving not just what they pursue, but also how they pursue it.

Insight 2

Growth drives strategic decisions, but priorities and actions vary significantly.

How leaders evaluate decisions and ultimately execute strategy are related but distinct processes, each influenced by a company’s decision-making mindset, industry context and scale. Examining the various catalysts provides a more complete view of how growth ambitions translate into real-world outcomes in the middle market.

DECISION-MAKING FACTORS

The pursuit of growth opportunities drives strategic decision-making in the middle market: across all mindsets, a majority of companies say it is a top-three consideration, with 30% of all companies saying it is the number one factor in their decisions.

Beyond growth opportunities, there is less consensus on the other factors companies evaluate when making strategic decisions. Overall, competitive pressure and talent availability are distant second- and third-place considerations.

Meaningful differences emerge in how the different mindsets weigh the other decision-making factors. The Performance Protectors are most likely to consider margins and market uncertainty, while the Centralized Innovators emphasize talent availability and are among the most likely to factor in risk mitigation and geopolitical factors. Disciplined Growers also place relatively high priority on risk mitigation. Decentralized Accelerators make up the group most concerned with the regulatory environment and geopolitical factors.

THE IMPACT OF INDUSTRY ON DECISION-MAKING FACTORS

Decision-making factors vary meaningfully by industry. Real estate companies are most likely to carefully consider market conditions and financing costs, while construction and consumer and industrial products businesses are more concerned with what their competitors are doing and if they can find the talent they need to move their organizations forward.

ACHIEVING OBJECTIVES

When it comes to achieving strategic goals, most companies agree they need to improve their profits, increase their sales and improve efficiency. Technology matters too, and making the right investment in this area is becoming increasingly critical and often directly related to efficiency gains. For example, many companies report using AI to drive efficiency across functions, including operations, HR, customer service and finance.

As with decision-making factors, key differences emerge among different mindsets and industries as to what is most important to realizing desired outcomes:

- Disciplined Growers - See investing in technology and attracting and retaining key talent as especially important to realizing their strategic objectives.

- Performance Protectors - Are more likely than other groups to emphasize reducing operational costs and attracting and retaining key talent as essential to executing strategy. They also place importance on expanding market share.

- Centralized Innovators - Stand apart in their commitment to investing in technology, developing new products and services and expanding into new markets to help drive outcomes.

- Decentralized Accelerators - Are more likely than their peers to focus on strengthening brand reputation, optimizing capital structure and improving cash and are notably less concerned with reducing operating costs and attracting and keeping talent.

THE IMPACT OF INDUSTRY ON EXECUTION

Margins matter most in the consumer and industrial products industry, while construction companies focus more on making every sale and relatively less on efficiency. Developing people is important in real estate; attracting and retaining people are key in construction.

MORE THAN ONE PATHWAY LEADS TO SUSTAINABLE GROWTH

Ultimately, growth ambitions set the direction in the middle market, but the pursuit of growth is not the sole determinant of how companies operate or perform. Differences in decision-making factors and execution priorities around issues, including financial discipline, talent and modernization, underscore the importance of mindset and operational context in translating growth opportunities into sustained performance.

Insight 3

Tradeoffs reveal where leaders are aligned—and where they are not.

Because resources are finite in the middle market, tradeoff decisions are a constant reality—particularly around talent, growth and costs. Leaders routinely must choose between growth and profitability, cost and quality, and employee workload and payroll size, among other competing priorities. Perhaps because these decisions are so common, most leaders in our study (87%) express high confidence in their decision-making ability.

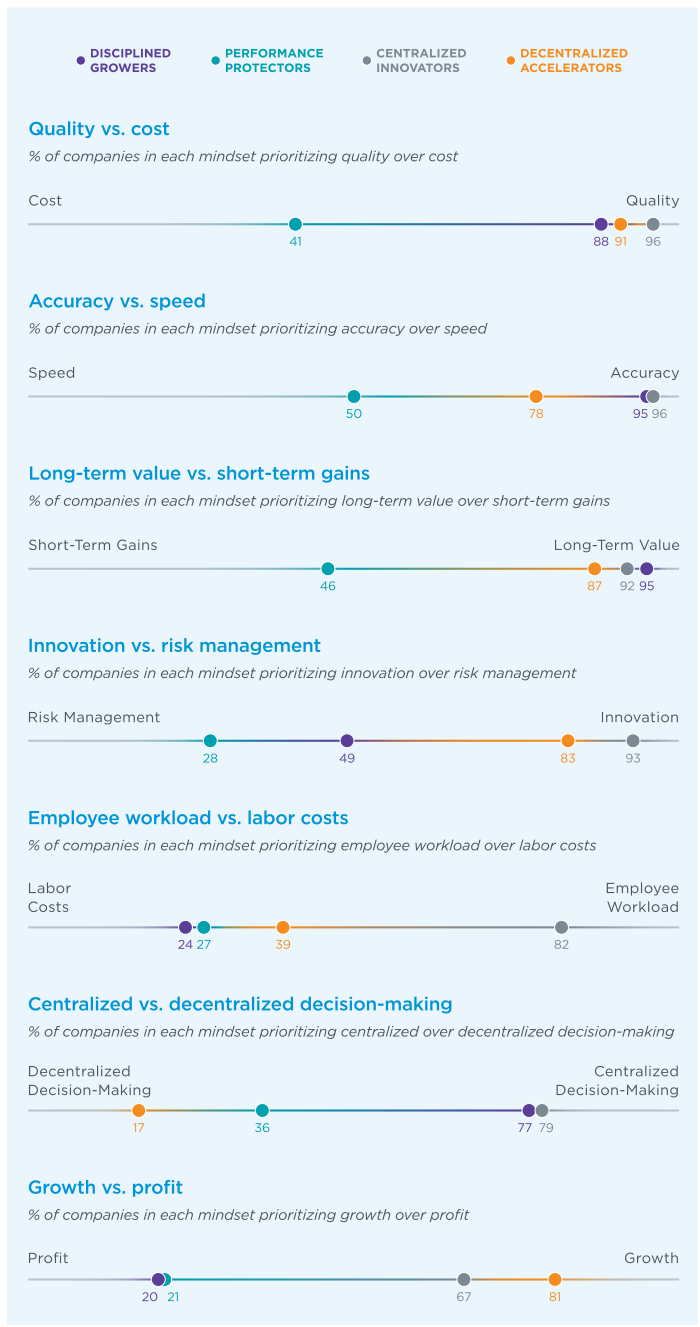

Across several foundational tradeoffs, the middle market shows strong alignment:

Across other tradeoffs, however, divergence becomes much more pronounced, both across the middle market overall and among the four decision making mindsets.

TRADEOFF DECISIONS DIVERGE WHEN CONSIDERING LEADERS’ MINDSETS

COST, SPEED AND TIME HORIZON

In all these tradeoffs, the outliers are Performance Protectors. Within this mindset, a meaningful share of companies favor cost, speed or short-term gains in their decision-making.

INNOVATION VS. RISK

When forced to trade off innovation and risk, 56% of companies surveyed say they would prioritize innovation over a safer or more balanced approach. Performance Protectors are most likely to manage uncertainty first, with only 28% saying they would opt for innovation over a safer approach. However, more than a third of Disciplined Growers also share this view. Not surprisingly, nearly all Centralized Innovators favor pursuing new advances.

WORKLOAD VS. COST/CENTRALIZED VS. DECENTRALIZED DECISION-MAKING

Tradeoffs related to people reveal even sharper differences. Our data shows that nearly half of companies (47%) prioritize labor costs, while 38% (predominantly Centralized Innovators) focus on managing employee workload. Decision authority also varies widely: 54% prefer centralized decision-making, while 27% lean toward empowering individuals, with Decentralized Accelerators dominating the latter group. Performance Protectors, notably, are also less likely to favor a centralized approach.

GROWTH VS. PROFITABILITY

Perhaps most interestingly, while growth opportunity is the primary factor shaping strategic decisions, among the companies we surveyed, more overall (47%) say they would prioritize profitability over growth (40%) when forced to choose one or the other. It is important to note that the two most prevalent mindsets—the Performance Protectors and the Disciplined Growers—are driving the split. Both the Centralized Innovators and, especially, the Decentralized Accelerators overwhelmingly favor growth, with 67% and 81%, respectively, choosing growth over profit.

DIFFERENCES INTENSIFY WHEN TALENT, RISK AND MARGINS ARE AT STAKE

These tradeoffs highlight a key distinction across the middle market: while leaders largely agree on foundational principles, they diverge when decisions directly affect people, risk profile and growth posture. The choices leaders make ultimately define and differentiate the four decision-making mindsets and how each balances competing priorities in practice.

Insight 4

When cost pressures force protect-or-sacrifice decisions, leaders differ on what is most essential.

Cost pressures remain a defining challenge for the middle market, forcing frequent tradeoff decisions. When faced with the need to cut costs, middle market leaders must decide what to protect and what to sacrifice. According to the survey results, companies show alignment in some areas: nearly half (49%) say they would protect customer service or customer experience, while only 25% would sacrifice it. At the same time, middle market leaders are far more willing to reduce investment in research, development and innovation, with 53% indicating they would sacrifice these areas and just 31% naming R&D as a top area to protect. While this overall pattern suggests a strong bias toward preserving near-term customer relationships, even at the expense of future-oriented capabilities, meaningful differences emerge across the four decision making mindsets.

DISCIPLINED GROWERS

Disciplined Growers place their highest priority on hiring and retaining talent. Compared with other groups, they’re more willing to sacrifice technology investments in order to preserve the workforce they view as critical to maintaining operational discipline and long-term performance.

PERFORMANCE PROTECTORS

Performance Protectors are significantly more committed to protecting risk preparedness and organizational resilience than the other mindsets. Notably, however, they’re also the most likely to sacrifice cybersecurity, signaling a distinction between traditional risk management priorities and investments tied to emerging or less visible threats.

CENTRALIZED INNOVATORS

Centralized Innovators stand apart in their priorities. Unlike the broader middle market, these companies are most committed to protecting technology investments, even at the expense of customer experience. This suggests a belief that sustained competitiveness and growth depend on continued investment in enabling platforms, systems and capabilities, particularly during periods of constraint.

DECENTRALIZED ACCELERATORS

Decentralized Accelerators demonstrate relatively stronger commitment to R&D compared to their peers. Marketing and brand rank high on their list of investments to protect. At the same time, they’re the most likely of all groups to sacrifice risk preparedness, underscoring a greater tolerance for uncertainty in pursuit of expansion.

WHAT LEADERS PROTECT REFLECTS THEIR DECISION MAKING MINDSET

Under pressure to cut costs, leaders reveal not just their priorities but their underlying beliefs about where value is created, how risk should be managed and which capabilities are most critical to sustaining performance over time.

Insight 5

Innovators experience stronger growth and greater confidence.

Among the four decision-making mindsets, Centralized Innovators post some of the strongest results across key performance indicators, including year-over-year revenue growth, employment growth, confidence in decision-making, competitive position and future prospects. Nine out of 10 Centralized Innovators report year-over-year revenue increases, with 51% growing by 10% or more. Nearly seven in 10 expanded their workforce over the past 12 months, and 46% did so at a rate of 10% or higher. Nearly all Centralized Innovators view themselves as ahead of their competitors and have strong outlooks for the next six months.

Decentralized Accelerators are a close second on most measures, while Disciplined Growers and Performance Protectors show more moderate growth patterns and confidence levels. Overall, middle market leaders who approach decisions through an innovation-oriented mindset consistently outpace their peers, suggesting a strong relationship between innovation-driven decision-making, higher performance and greater confidence in both current positioning and future outlook.

EXECUTION MATTERS, TOO.

While innovation is correlated with growth, it is not the only factor associated with fast-growing businesses. Importantly, several characteristics cut across mindset when examining the fastest-growing companies in the study—those achieving year-over-year revenue growth of 10% or more.

Compared with slower-growing peers, these are more likely to:

1. Place greater emphasis on strengthening brand and reputation and optimizing capital structure

2. Invest in their people through training and upskilling (52% vs. 43%), attracting and hiring qualified talent (49% vs. 39%), and leadership development (36% vs. 26%)

3. Prioritize data privacy investments (37% vs. 26%)

4. Report significant efficiency gains from investments in automation or process improvement (45% vs. 17%)

5. Maintain a long-term growth orientation (61% vs. 49%)

In the middle market, performance at the highest levels reflects disciplined execution across marketing, talent development, financial management and operational excellence, suggesting that sustained growth is shaped by a combination of mindset and fundamentals.

Special Feature: How Middle Market Leaders React when Growth Comes at a Cost

A Window Into Decision Behavior

To better understand how middle market companies approach tradeoffs under pressure, we asked leaders how they would respond to a hypothetical market opportunity promising strong growth but requiring a 12% increase in operating costs.

The Scenario Provided to Respondents:

Your company has the chance to expand into a new high-growth market where competitors are weak. To seize the opportunity, you must immediately increase operating costs by 12% to hire local talent, adjust supply chains and increase marketing.

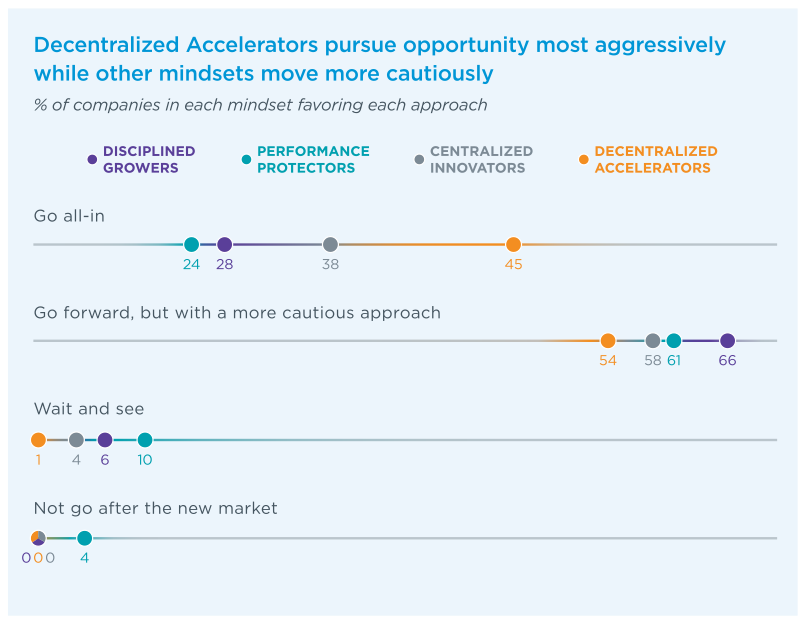

MOST LEADERS WOULD PURSUE THE OPPORTUNITY—BUT WITH MEANINGFUL GUARDRAILS

Nearly two-thirds (61%) say they would move forward carefully, while around a third (32%) would go all in. Companies willing to fully commit tend to be larger—upper middle market companies are twice as likely as lower middle market companies to go all in. They are also faster growing and more confident in their competitive position and decision-making capabilities. They take a long-term, often automation-enabled approach to growth. This profile signals a greater ability and willingness to absorb cost increases today in pursuit of long-term gains. By contrast, more cautious leaders emphasize control, staged investment and near-term cost protection.

MINDSET SHAPES RESPONSE AND SPEED OF COMMITMENT

Decision-making mindset strongly influences how leaders react to opportunity.

Disciplined Growers - These

decision-makers deliberately avoid overcommitment, with two-thirds

pursuing the opportunity with measured changes; 6% would wait and see.

“We like to take advantage of opportunities when they arise, but

we are also somewhat cautious as to not completely go all in without

some barriers. We set budgets and limits for such opportunities.”

– Real Estate, Lower Middle Market

Performance Protectors - This group seeks optionality. While around a quarter would go all in, most would proceed cautiously. One out of 10 Performance Protectors would adopt a wait-and-see posture, and 4% would opt out entirely.

“We would want to see if the market opportunity is not transitory, and we are able to have a higher level of confidence as to the benefits before proceeding with such a high investment.”

– Consumer and Industrial Products,Upper Middle Market

Centralized Innovators - Leaders with this mindset would advance more quickly but continue to skew toward governance and control.

“These are times when competitors are more cautious, and we’ve found these are times where we can succeed and bring our strengths to the table as a challenger company.”

– Construction, Lower Middle Market

Decentralized Accelerators - Decision-makers in this group act most decisively when growth is available, even at material cost. Nearly half (45%) would go all in, making this group the most likely to seize the opportunity.

“The window of opportunity is short, so we must quickly seize market share and build brand awareness, even if it means increased costs in the short term.”

–Consumer and Industrial Products, Upper Middle Market

CBIZ Perspective

Growth With Clarity: Strengthening Decision-Making in the Middle Market

By Brad Lakhia, Chief Financial Officer, CBIZ

Middle-market leaders are highly entrepreneurial and ambitious. Our research makes that clear. Confidence is high, and growth is a top priority across industries. But when uncertainty and tradeoffs get expensive, hesitation creeps in. Leaders pause when margins tighten, hiring demands higher wages, or technology investments require short-term sacrifice for long-term gains.

That pause is understandable. Middle-market companies don’t have similar safety nets of global scale or deep, cost-effective access to capital. They manage volatility in real time, protecting people, customers, margins and their own capital because those decisions carry significant consequences.

But the data and findings reveal something worth considering further. Companies that lean into innovation and are more decisive consistently post stronger revenue growth and report higher confidence in their competitive position. That pattern isn’t a coincidence.

At the same time, protection, discipline and careful judgment serve a legitimate purpose. They build resilience. They preserve stability. They safeguard what middle-market companies have worked hard to build.

CLARITY SHAPES BETTER DECISIONS

In our experience, what separates top performers from more cautious companies is rarely ambition — it’s clarity. Leaders with deep visibility into their financial performance, workforce economics, operational capacity and risk exposure make stronger decisions. Not because they’re more aggressive, but because they understand the full picture. When insight integrates across the business, tradeoffs stop feeling like leaps of faith and start feeling like deliberate choices.

That is where many middle-market companies need a more structured process.

Better tradeoff decisions should not sit with one function alone. The CEO or owner sets priorities and risk tolerance. The CFO helps evaluate the financial, tax and cash flow implications. The broader leadership team tests those choices across operations, workforce, technology and risk. In the middle market, better decisions are cross-functional decisions.

WHERE LEADERS CAN START

For leaders wondering where to start, begin with alignment on the few measures that matter most. Revenue potential matters, but so do margin impact, cash requirements, workforce capacity, execution risk and time to return. Without that shared lens, growth decisions can drift away from what the business can realistically support.

Next, create a more integrated view of the business. Many middle-market companies still review tax, workforce planning, modernization and risk separately, making tradeoffs harder to evaluate. Leaders need to understand how one move affects another. When those issues are considered together, decisions become clearer.

Finally, establish a regular leadership cadence around major investment and operating decisions. It does not need to be complex, but it should be consistent. A cross-functional review process helps teams pressure test opportunities, spot blind spots and align resources before decisions become reactive.

STRENGTHS AND BLIND SPOTS FOR EACH MINDSET

The research highlights four decision-making styles, each a reasonable response to pressure. Performance Protectors focus on costs and resilience. Disciplined Growers balance growth with control. Centralized Innovators modernize in a structured way. Decentralized Accelerators empower teams to move quickly. No style is inherently better; each delivers results when applied in the right context.

What really matters is whether leaders can spot the blind spots that come with their usual approach. Focusing too much on protection can hold back investment in new ideas. Moving too fast can compromise important checks and risk planning. Being too careful can lead to missed opportunities. And if speed is not managed, it can create more complexity and problems over time.

Middle-market companies don’t have to pick between stability and progress. Those that grow sustainably tend to align their financial insight, tax planning, workforce management, modernization and risk control into a single set of connected decisions, not separate tasks. When leaders look at these areas together, tradeoffs are easier to see, and the way forward is clearer.

The research shows that leaders who prioritize innovation often outperform in both growth and confidence. It also finds that most organizations value long-term results, quality and culture. The real differences appear when decisions affect people, profits and risk. Those are the moments when clarity isn’t just an advantage, it’s the difference.

CONNECTED INSIGHTS CREATE BETTER TRADEOFFS

Middle-market companies do not have to choose between stability and progress. The businesses that grow more sustainably are often those that align financial insight, tax planning, workforce management, modernization and risk oversight into a single, connected set of decisions and use them together to guide action.

At CBIZ, our focus is on helping companies bring those insights together by evaluating investments, identifying hidden constraints and strengthening capabilities that may not come naturally to their existing mindset. With that kind of integrated thinking, leaders can better understand the operational and financial impact of their choices. The goal is not to become more aggressive for its own sake, or more cautious for comfort. It is to become more informed, more coordinated and more deliberate. When leaders can see tradeoffs clearly and evaluate them through a connected lens, they are better positioned to protect what matters today while investing in what will matter next.